Due to the recent pandemic, people were forced to be locked down in their own houses or apartments for a very long time. This caused a massive unemployment, business closure and disinterest in investing – even for the home of their dreams. The property market is just one of the markets that has been greatly affected by this. Let’s find out if these factors led to an increase or decrease to the current house price in the UK

Cost of Housing

In the start of 2009, the lowest house price in the United Kingdom was reported with an average of 157.2 British pounds. Since then, there was a remarkable and steady increase in the prices of houses. In 2013, the house prices increase quarterly and by the latest statistics last February 2020, the prices of the houses in the UK was about 230.3 thousand British pounds. In the past 13 years, it is between 2013 and 2014 where the highest house price was recorded at 9% increase.

Cost of Renting

For those who are not yet ready to spend a lot of money to buy a home opted to rent a home. Many people rent homes in big cities because of the bigger opportunities in their career. The downside of it though is that the cost of living is high too making it difficult to save some money for buying a real estate property. On the brighter, this increases the demand for affordable residential homes in the city boosting its property market.

House Price

When there is a presence of an economic uncertainty due to such unpredictable factors – like the coronavirus, we expect the house price to decrease. Since the lifting of the lockdown restrictions, many businesses and sectors are trying to gain their losses in the previous month. The property market is slowly getting back on track while implementing safety measures.

The average house price in the United Kingdom in 2007 is just 176, 758 British pounds while the latest data shows that in February 2020, the house price is about 230,332 British pounds. The peak of house price was seen between 2013 and 2014 where the prices had a 9% increase.

At the start of 2020, it was predicted that the prices of properties on sale will significantly rise due to the number of people who are searching for homes from towns and city centers. Many are looking for a home with a wide garden and has a good amount of space where they can put up their own home office. But since the unexpected pandemic, many people temporarily put their house hunting on hold and are focusing on how to get by while the economy is still unsure.

According to experts there are two scenarios that can happen due to this. First, property prices may fall but it is still good to invest in it as it is considered to be a long-term investment and may even give you a good return in the future. Second factor is the flexibility of the property market which was proven overtime. Many factories and buildings were redesigned to be condominiums or residential areas. This setback is just temporary and will probably go back to normal once the massive shock caused by covid-19 is gone.

Planning to get an interest-only mortgage loan? You may have to think about it again. You need to consider not only the expenses but also how long you are willing to pay for the mortgage. We will discuss the advantage and disadvantages of interest-only mortgage. Get to know if this type of financing is an option for you.

Interest-Only Mortgage

An interest-only mortgage is a type of mortgage wherein the borrow is only required to pay for the interest on the loan for a certain period of time. Then, the principal will still be repaid either through giving a lump sum at a certain date or through subsequent payments.

In interest-only mortgage, the borrower only pays for the interest through monthly payment for a fixed term. The term usually last for 5 to 7 years. Many take this loan and after paying, they refinance their home or give a lump sum payment to pay-off the principal loan that is left.

People who often take-out this loan are the borrowers who currently desires to afford more home, knows that the home they bought will be easily sold within the next few months, some who wants the initial payment for the mortgage to be significantly lower as they are still starting but are confident that they will be able to deal with the large amount of payments in the future and lastly, those who are really certain that they will be able to get a significantly higher return of investment somewhere else.

Advantages And Disadvantages

Like any other type of loan, the interest-only mortgage has its pros and cons. The advantages of Interest-only loan are the following:

The monthly payment terms are low during the whole term.

The burrower can actually buy a larger home later due to the higher qualifying loan amount.

You have free use of the money and you can invest it in to gain higher investment.

In the interest-only period, the amount you are paying monthly qualifies as tax-deductible.

Let us also look at the disadvantage of such mortgage terms:

It also increases the rising mortgage rate if it is an ARM.

People do not use their money smartly and often spend their extra money instead of putting it on a good investment.

At the end of the interest-only mortgage, many people are unable to pay for the principal amount which tends to increase gradually.

Many borrowers are not also disciplined enough to pay on time and tends to give extra payment towards the principal.

Some investments may not grow as quickly as it ought to be and ruins some payment plans.

The mortgaged home’s value may not appreciate as fast as they thought it would be.

It may cause “payment shock”, due to the significant increase on the principal payment which the borrower may have forgotten in time.

Is Interest-only Loan for You?

This loan scheme may have its risks but some may find it terms applicable in their current life and in their future plans. You should be able to fulfill the following qualities in order to apply for this type of loan:

You have a decent income which will surely increase as years go by.

The mortgaged home has a good equity and the borrower can actually use the money to pay investments and even principal payments.

Lastly, if your current job does not pay good and you want a flexibility of paying only the interest at this time then you may also consider this. If your income increases in the years to come, then you are good to go.

Interest-only loan is not as bad as it sounds but people often misuse it. If you have a good plan and strategy for your mortgage and you think you can actually put it out into action in the next coming years, then this might be a good choice for you. It is important for you to know and understand the difference between the actual benefits it brings and the temptation from having to pay a lower payment. Takeaway: Do not buy more than you can afford.

With the pandemic still present, the economy is still struggling due to keep up with the losses caused by it. One of its great impact is on the real estate industry. The decrease in the number of people looking for a new place and the limited movement brought about by the previous restrictions due to COVID-19 greatly decreased the income of real estate companies causing a downward trend to the prices of properties.

Negative Equity

Negative equity happens when the value of the real estate property under mortgage is worth less than the mortgage secured on it. This often occur when the property prices are falling due to a recession or an economic depression. Negative equity is calculated by simply knowing the current market value of the property and subtracting the amount remaining on the mortgage. For example, if you bought a property for £200,000 with a mortgage for £ 180,000 and now the market value of the property is only £ 150,000 then you will be in negative equity. This is not good news for real estate agents and borrowers as it decreases the market value and their possible income from selling these properties.

Economic Implications

As negative equity happens when a person bought a house prior to a depression or recession, in this case the unpredicted COVID-19 pandemic, causing the current market value to be below the mortgage. They also use the term “underwater” to refer to borrowers or property owners as having a negative equity if they want to sell their properties at this time.

Negative equity has been a common problem of homeowners during the 2007-2008 financial crisis. Homeowners were affected by this found themselves unable to actively pursue work in other states or areas because of the potential losses that they can incur from the sale of their homes.

Selling a Home

If you are planning to sell a property, now may not be the best time as property prices are falling. Unless you have an available savings in the bank or investments that you can use to repay the difference between the market value and the mortgage, then you might find it difficult for you to move to a different place, state or country. Some banks may offer remortgage, but you may have a hard time finding one or if you find one, they might have a fixed rate.

Pros and Cons of Negative Equity Mortgage

Pros:

Moving houses does not require you to pay off the negative equity on your mortgage. This particularly useful if you really need to move and you can’t stop it.

Cons:

Moving might cause you to pay your repayment charges early on your existent mortgage.

Fees and charges may be added, and a new mortgage might have a higher interest rate compared to the previous one.

There are only a limited number of lenders that offer this type of scheme and they often have different requirements before they approve your mortgage.

Reduce your Negative Equity

Reducing your negative equity is possible. This is done by simply overpaying the monthly amount due on your current mortgage. Before doing this, make sure that your existing mortgage accepts overpayments and if so, how much can you add to your payment without incurring an early repayment charge. Make sure to keep your income or savings in check prior to doing this as it is and added expense.

Renting out

If you don’t need immediate money but would like to move due to some personal reasons, you can consider renting out your home. This means that you are still keeping and paying the existing mortgage, but it may have a higher interest than your usual.

During this time, the whole world is suffering from the consequences that the COVID-19 virus has caused us. Many people were laid off from their jobs because a lot of businesses has closed down due to loss of income. People are having a hard time paying mortgages and earns a lot of debt because of this. So, what is mortgage write down and how can it potentially help the struggling homeowners?

Mortgage Write Down

So what should you know about mortgage write down? Mortgage write down happens when a borrower sends a letter to the lender with the intention of offering a viable alternative for their payment terms due to financial constraints. It usually occurs when a lender reduces the principal owed on one of its mortgage loans as a consideration for the financial difficulty that the borrower is experiencing.

Last May, many banks has set out details of Covid-19 mortgage holidays for the household who was hit pretty badly by the coronavirus making their finances unstable. This is designed by the banks for the borrowers to overcome the temporary income shortfall that no one predicted. A three-month extension for mortgage payments is enough of help for the people currently struggling financially.

Will the Bank Write Off your Debt?

With a debt write down or an informal arrangement with the bank, both the lender and the borrower will need to have an agreeable and affordable sum that will somewhat make it easier for the borrower to pay without compromising their credit value. Some people who are new to this can be quite skeptical about it and wonders why the bank would ever consider this agreement for the debt. Here are some reasons why the bank does so:

The bank does not want to repossess the property they already “sold” to the mortgager. Instead of repossessing and gaining an empty property again with no value or sells 20% less than their true value, they would rather talk it out with the borrower and have an agreeable amount. This will both be beneficial for the borrower, because they can continue paying for their mortgage, and the bank, for getting payments for the mortgaged property.

Having a hard time to make ends meet due to recent unexpected events is expected. If you’ve fallen into arrears and not able to pay your mortgage repayments, you can expect to receive letters from the lenders or the solicitors warning that they could take this matter to court which banks does not really want to do as it costs a lot of money.

Once the bank repossesses the mortgaged property, they cannot sell it again on its true market value. Because of this, they sell it on a discounted price significantly losing some money in the process.

If you and the bank didn’t get to reach an agreement, they can’t easily take back the mortgage property. They need to properly follow the protocol for this which not only costs a lot of money for the legal aspects but also takes a lot of time.

Struggling to Make Payments?

It is expected that a lot of people are having a hard time balancing their finances because of the recent events. Depending on your payment history, you may try if the lender will agree to:

Reduce your payments for a set period – show them a proof of your current income and expenses and how much money you can shell out for the mortgage. This will make the lender understand your case and might consider giving you a Mortgage write off.

You can also ask them to charge you only the interest for the time being, if you have a repayment mortgage. This usually ask you to pay for capital and interest.

Some banks already said that they are giving out payment holidays where you can apply.

Lastly, try to extend your mortgage term to reduce your payments. This is ideal for someone who is not sure whether their finances will be stable for the next coming months. The only downside of this is it also prolongs the payment and increases the interest.

There are many different ways to get help if you are having difficulties in paying your mortgage. If you have extra money or other source of income, you can try to reduce your expenses by re-checking your finances and continue paying for your mortgaged property.

With the whole world undergoing a crisis because of the pandemic caused by COVID-19, how is the real estate industry going to be affected? Is the UK ready for a price crash of estates on sale?

The Property Market

Property markets are beginning to open particularly in England, Scotland, Northern island and Wales somehow relaxed its restriction. This means that in-house viewings have started once again and that buyers all over UK are able to buy a house and move from one place to the other.

There is a rough estimate of about 700,000 moves within the UK for the year 2020 but there was a 3% decrease as compared to a year ago. About 1/8 of the buyers opted to put off moving because of the recent lockdown. The present pandemic situation makes the people uncomfortable with moving and are waiting for further developments before continuing their plans.

Are the House Prices going to Change?

a saleswoman or estate agent shows a couple around a home with new kitchen

It might be too early just yet to predict an upcoming house price crash but with the recent figures reported, the prices are currently going down. House prices growth reportedly fell from 3.7% to about 1.7% last May.

Prior to the lockdown, the real estate market has been growing quite steadily with economic provisions that aims to support the industry. After the lockdown, the safety measures and limits set by the government has a great impact on the flow of housing transactions. It is expected that this trend will go on for some time until the people became comfortable and the economy recovers from the side effect of the pandemic.

There are different predictions as to whether the property market will be able to bounce back relatively fast after this setback. Majority of these predictions says that there would be a cold price drop by at more or less than 5% this year before seeing the light again on 2021 and increase by about 1.5% to 3%.

The Struggling Borrowers

The lockdown caused millions of jobs to be paused hence the flow of income within a household is cut. The Financial Conduct Authority (FCA) announced last month that the borrower’s mortgage payment holiday will be extended further for 3 months or their payments can be made staggered. This is to help those who are financially unstable due to the coronavirus.

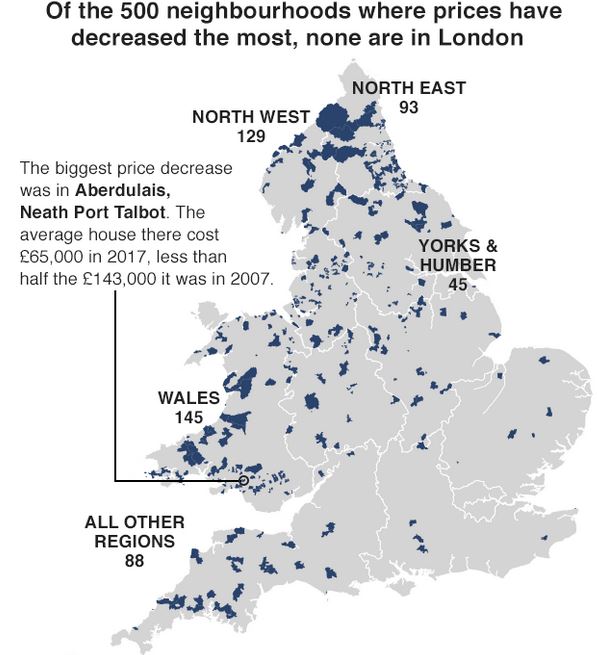

BBC have written an article on Negative Equity and have concluded that, in 58% of areas, homes are selling for less now than they were in 2007 (although this also factors in price growth due to inflation).

Interesting report on the BBC today about how RICS (Royal Institution of Chartered Surveyors) is viewing the latest property market. The headline says ‘property market stagnating’ but what does that really mean? The cause for this headline is the latest monthly data on stock levels – ie houses available for sale.

on average, each estate agent has just 43 properties for sale on its books, the lowest number recorded since the methodology began in 1994

They also say that the number of people registering to buy and the actual number of sales is way down. They did say however

because of the shortage of housing, it said prices in many parts of the UK are continuing to accelerate.

As usual there is a north/south divide with prices dropping in central London but being quite strong in the North West.

There is no sign of immediate relief

“For the time being, it is hard to see any major impetus for change in the market, something also being reflected in the flat trend in transaction levels.”

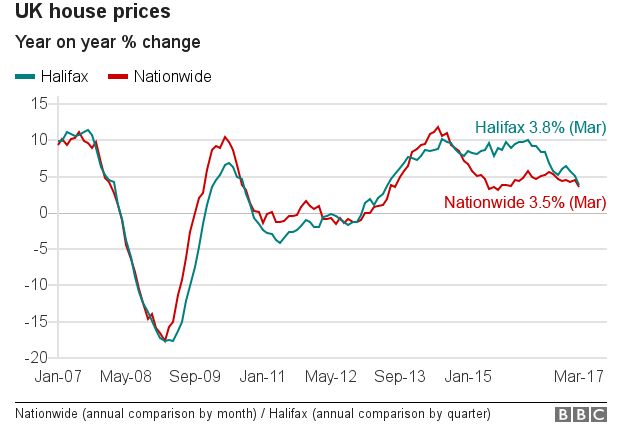

Earlier this week, the Office for National Statistics said house prices grew at 5.8% in the year to February, a small rise on the previous month. However, both Nationwide and the Halifax have said that house price inflation is moderating.

When putting pen to paper to buy a new home, most people expect to know how much they will need to pay to own it outright. But thousands of families in England and Wales are discovering the new-build houses they bought are not all they seemed.

Katie Kendrick bought her new-build home from Bellway in Ellesmere Port, Cheshire, three years ago for £214,000.

“It was supposed to be our forever home,” she tells the BBC’s Victoria Derbyshire programme, sitting in the living room of her four-bedroom house. “But it’s the biggest mistake I’ve ever made.”

Katie knew the house was leasehold – meaning she owned the property for the 150-year length of her lease agreement – but claims she was told by the sales representative that because of the long lease it was “as good as freehold”; a property owned outright.

She thought nothing of it, and says she was told she would be able to buy her freehold after two years, believing it would cost between £2,000 and £4,000.

But a year and a half later, she received a letter from Bellway saying her freehold had been sold to an investment company, which was now quoting £13,300 for her to buy it.

“At the moment I feel completely blind and in a corner and don’t know which way to turn. There’s legal action but that is very costly,” she says.

Leaseholds and freeholds

A freeholder of a property owns it outright, including the land it is built on.

Most houses are freehold but some might be leasehold – usually through shared-ownership schemes.

With a leasehold, the person owns the property for the length of their lease agreement with the freeholder.

Leaseholders have to pay their freeholders ground rent and other fees in order to make changes to their homes.

When the lease ends, ownership returns to the freeholder unless the person can extend the lease.

Some wish to buy their freeholds to save themselves these costs.

Source: The Money Advice Service

What Bellway has done – selling a new home as leasehold, and then selling the freehold separately to an investment company without informing the family living there – is not illegal.

In England and Wales, the “right of first refusal” applies to flats, but not houses. So it was not legally obliged to tell Katie it would do this.

For an investment company, buying groups of freeholds is a safe long-term investment. Receiving regular payments for ground rents – over leases that number well over 100 years – means safe, steady incomes, to fund things like pensions.

The campaign group Leasehold Knowledge Partnership estimates this business is worth up to £500m to the developers each year.

The leasehold system has existed for a long time in England and Wales, especially in blocks of flats. Many leaseholders have long leases, for example for 999 years, and experience no problems.

But the trend for new-build houses being sold as leasehold has accelerated in recent years. While not all house builders use this model, those that do argue it helps make developments financially viable.

But nowhere on Bellway’s website is this system made clear to potential buyers, and Katie feels these facts were not made clear to her. She also says the solicitor – recommended to her by Bellway – made no mention of this possibility either.

Katie says because she bought the house through the government’s Help To Buy scheme, she felt she could trust the process.

Bellway has not responded to requests for comment.

Homeground – the company that now manages Katie’s freehold on behalf of the investment company – said in a statement it “can usually informally negotiate a price which can often save both time and some of the professional fees”.

“In the rare event we cannot agree, the leaseholder still retains the right to turn to the statutory process, which will establish the price as well as the legal fees they have to pay.”

‘It’s immoral’

It’s likely thousands of homeowners could be in a similar position to Katie. Lindsay, who lives on the same estate, bought a house from developers Taylor Wimpey.

The company did ask Lindsay if she wanted to buy her freehold – for £2,600. She declined because she was on maternity leave and felt financially it was not possible.

Two years later she asked about buying it but found it was now £32,000.

“I rang them and said, ‘I’d like to buy it now.’ And they said, ‘It’s not for sale – there’s a private investor who owns it. They’ve got a long-term interest in your property,'” Lindsay explains.

“I turned around and said, ‘I’ve got a long-term interest in my property. It’s my family home, it’s my son’s inheritance, and it’s not yours to just line your pockets with.’

“I feel like I’ve let everybody down because it wasn’t right to buy it when it came. But nobody said this was a one-time offer.

“It might be legal, but it’s not even questionable that it’s immoral,” she adds.

Taylor Wimpey said as it no longer owned the freehold to Lindsay’s house, it did not set the price of the freehold or benefit from the ground rent.

It added that, since the start of this year, houses on its new developments would be sold as freehold-only, except in a small number of cases where it did not own the freehold to the land.

But other developers are still selling new-build houses as leasehold.

Katie and Lindsay do have the option to negotiate with the companies who own their freeholds, but say they do not wish to go down this route. They feel the original prices should still stand.

The law does allow a leaseholder to force their freeholder to sell after two years – if both sides cannot agree a price, a tribunal will decide how much the leaseholder should pay.

However, the leaseholder can also be liable for the legal fees of both parties, meaning further expense to people like Katie and Lindsay.

‘Unsellable’

A spokesman for the Department of Communities and Local Government has told the BBC “it is unacceptable if home buyers are being exploited with unfair charges and unfavourable ground rent agreements prior to purchase.

“We are aware of this issue and will announce radical proposals to reset the housing market in our forthcoming White Paper.”

Beth Rudolf, from the Conveyancing Association, says that if the developers were not clear about the leaseholds, it may be a case of misrepresentation.

“Anyone marketing a property is covered by consumer unfair trading regulations, which means that if there is anything that would affect their decision-making process, then they should be advised of that before viewing the property,” she says.

“It’s too late when they move into the house to find that out, it’s too late when they become legally liable to purchase it.

“It’s too late really at the point when they’ve viewed it, because they’ve already fallen in love with it.”

The fight goes on for Katie and Lindsay, who worry their homes are now “unsellable” while this shadow hangs over them.

“Hindsight’s a wonderful thing,” says Lindsay. “I wouldn’t have done it if I had known.”

This article from the BBC shows how big household debt has grown in recent years. British families owe an average of £3,737 in loans and credit cards; plus their mortgage and rent payments.

While interest rates are low it’s not as big a problem for families as it might be. However as inflation rises post-Brexit pressure will be on the Bank of England to raise interest rates and that could greatly increase the cost of mortgages and other debt.

The part of the UK hit hardest by the negative equity trap is Northern Ireland. According to figures from mortgage administration company HML, 41% of borrowers in Northern Ireland who have taken out mortgages since 2005 owed more than their house was worth during the last quarter of 2013. That is the highest rate of 12 UK regions.

That’s an incredible 68,000 households whose properties are worth less than their outstanding mortgages. One bit of good news is that prices are rising slowly and this figure for those in negative equity has dropped from over 75,000 in the last quarter of 2013. Still it is small comfort to those who wish to sell their properties and move on. Particularly as some analysts are forecasting that it will be several years yet before house prices in NI catch up to their peak.

Check out this article in the Telegraph for more details.